Media Summary: Code files on Github: Program uses Mean-Variance ... demonstration for how to add more complicated constraints to solver so we still want to solve for optimized Ryan O'Connell, CFA, FRM shows you how to perform

Overview

Portfolio Optimization In Python The Math 2 3 - Detailed Analysis

Code files on Github: Program uses Mean-Variance ... demonstration for how to add more complicated constraints to solver so we still want to solve for optimized Ryan O'Connell, CFA, FRM shows you how to perform minimum variance portfolio, portfolio mathematics, matplotlib, numpy, Hello everybody now we will be going over the Watch this webinar, featuring Finor, to learn how

Buy me a coffee: Support me on Patreon: About ... Can you mathematically guarantee higher returns with lower risk? In 1952, Harry Markowitz proved you can. Here is the Dive deep into the world of financial computing with our comprehensive guide on Risk Analysis and

Gallery

Photo Gallery

![Quant Finance with Python and Pandas | 50 Concepts you NEED to Know in 9 Minutes | [Getting Started]](https://i.ytimg.com/vi/b9RgHa1CnH4/mqdefault.jpg)

Related

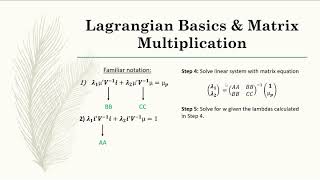

![PORTFOLIO THEORY with MATRIX ALGEBRA using Python: OPTIMIZATION [Part II]](https://i.ytimg.com/vi/hTfja2lu5zY/mqdefault.jpg)